Your credit score isn’t just pulled out of thin air—it’s built from data in your credit report and run through a scoring formula. The result is a three-digit number, usually between 300 and 850, that lenders use to decide how risky you are as a borrower. But how do all those pieces of information get turned into a single score? Let’s break it down in a way that’s easy to understand.

What Is a Credit Score?

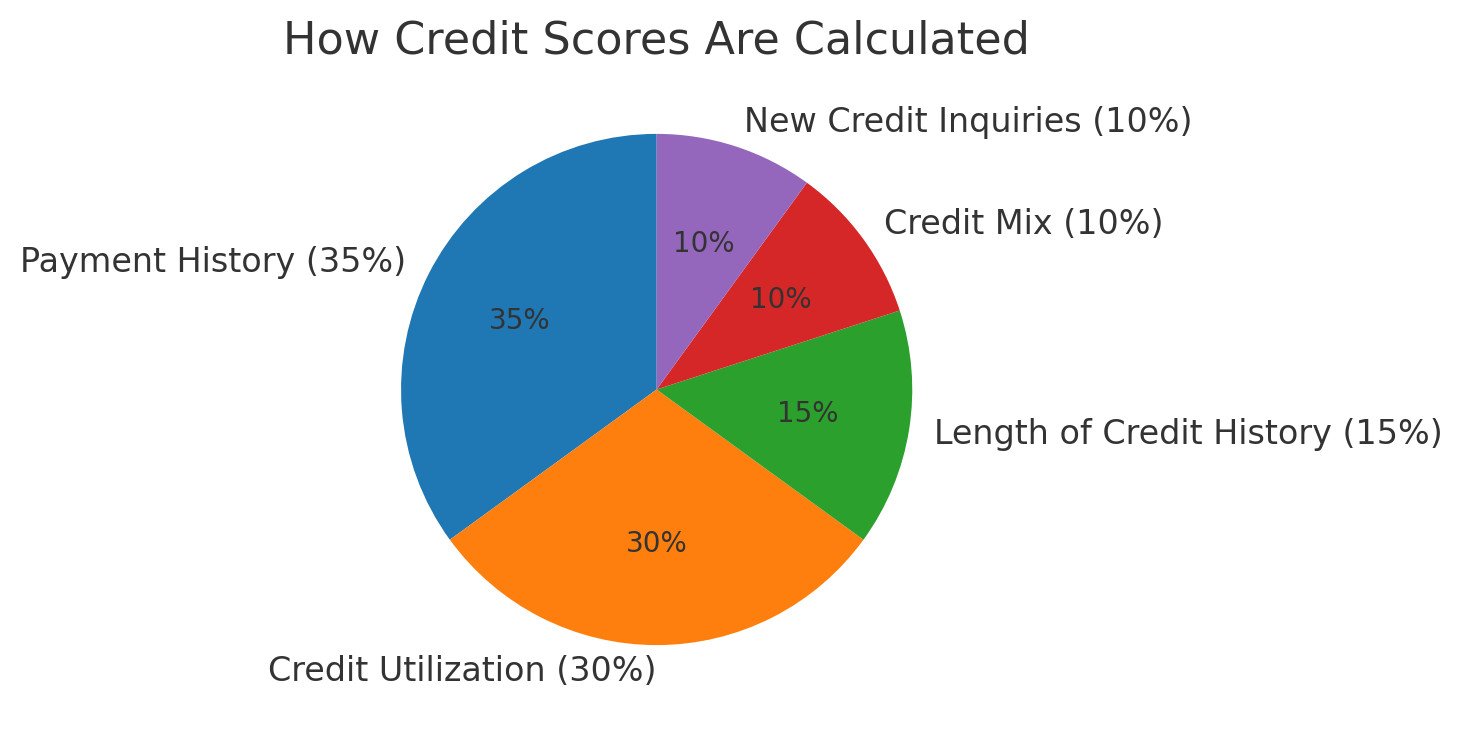

A credit score is like a financial GPA. Just like a school GPA is calculated using test scores and assignments with different weights, your credit score is calculated using categories of financial behavior. The most widely used score, the FICO Score, is based on five categories. Each category carries a percentage weight, and all those percentages add up to 100%. That weighted formula is what produces your number between 300 and 850.

The Five Categories in the Formula

Here’s how the scoring formula breaks down:

- Payment History – 35%

- Credit Utilization – 30%

- Length of Credit History – 15%

- Credit Mix – 10%

- New Credit Inquiries – 10%

But what does that really mean when it comes to calculating a final number? Let’s go deeper.

1. Payment History (35%)

This category looks at whether you’ve paid past accounts on time. Think of it like your biggest exam score—it has the heaviest weight. Even one late payment can drop your score because it’s calculated as a percentage of your total payment record. For example, if you’ve had 100 payments and missed 2, that’s a 98% on-time record. The better your percentage, the more points you earn toward your score.

2. Credit Utilization (30%)

This measures how much of your available credit you’re using. The formula looks at both individual cards and your overall usage. For example, if you have $10,000 in total credit and you’re using $3,000, your utilization is 30%. A lower utilization shows you’re not overextended. Keeping it below 30% is considered good, but those with top scores often keep it closer to 10% or less.

3. Length of Credit History (15%)

This factor isn’t just about your oldest account. It also includes the average age of all your accounts and how long it’s been since you last used them. The math here rewards people who have had credit open for many years. So if your oldest card is 12 years old, and you open a new one today, the average age of your accounts goes down, which can slightly lower your score.

4. Credit Mix (10%)

The formula also looks at the types of credit you have. Having both revolving credit (like credit cards) and installment credit (like car loans or mortgages) shows you can handle different financial responsibilities. If you only have one type, you won’t get the full 10% in this category, but it usually has a smaller impact compared to payment history or utilization.

5. New Credit Inquiries (10%)

Every time you apply for credit, it creates a “hard inquiry.” The formula counts these in the last 12 months, with fewer being better. Multiple inquiries in a short time can slightly lower your score, especially if you don’t have a long history. That said, credit scoring models group certain inquiries (like shopping for a car loan) together so they don’t penalize you unfairly.

Putting It All Together

Now, how does all of this become a number? Think of it as a pie chart that adds up to 100%. The scoring model looks at the data in your credit report, assigns each category its weight, and calculates how strong you are in each area. When all of those weighted sections are combined, the algorithm translates them into your final score between 300 and 850.

Example: How Someone Ends Up With a 720 Score

Let’s imagine Maria. She has several credit cards, a car loan, and a student loan. Here’s how her profile looks when the formula is applied:

- Payment History (35%): Maria has made 98% of her payments on time over the last 7 years. That’s strong but not perfect, so she earns about 30 out of 35 possible points in this category.

- Credit Utilization (30%): Her credit cards total $15,000 in limits, and she’s carrying $4,500 in balances. That’s 30% utilization, which is acceptable but not excellent. She earns about 20 out of 30 points here.

- Length of Credit History (15%): Her oldest account is 10 years old, but because she recently opened a new card, her average age dropped to 5 years. That puts her at about 10 out of 15 points.

- Credit Mix (10%): She has credit cards, a car loan, and a student loan. That variety is healthy, giving her nearly the full 9 out of 10 points.

- New Credit Inquiries (10%): She applied for two new cards in the past year, which is a little high. She earns about 6 out of 10 points here.

Add it up: 30 + 20 + 10 + 9 + 6 = 75 points out of a possible 100. When mapped onto the FICO scale (300 to 850), that works out to roughly a 720 score. This puts Maria solidly in the “good” credit range, though she has room to grow by lowering her utilization and avoiding new inquiries.

Why Credit Scores Matter

Your credit score affects more than just loan approvals. A higher score means lower interest rates, saving you thousands over time. It can also influence rental applications, insurance rates, and even job opportunities. In other words, improving your score doesn’t just boost your number—it directly impacts your wallet and opportunities.

How to Improve Your Score

The formula might sound complicated, but improving your score is really about practicing good habits consistently:

- Pay every bill on time.

- Keep credit card balances as low as possible.

- Keep older accounts open to build history.

- Only apply for new credit when necessary.

- Check your credit report for errors that could hurt your score.

Learn More

If you’d like to go deeper into the exact formulas and details, the Consumer Financial Protection Bureau (CFPB) has free resources to help you understand credit reports and scores in plain English.

Final Thoughts

Your credit score isn’t a mystery once you understand how the weights and categories work together. By focusing on the most important parts—on-time payments and low balances—you can steadily raise your score. And as your score goes up, so do your opportunities for financial freedom and savings.