If you’ve ever checked your credit report and noticed terms like “charge-off” or “collection,” you might wonder what they mean — and whether they’re the same thing. While both can hurt your credit score, they are actually different stages in the debt process. Understanding these differences can help you plan your next move and protect your financial future.

What Is a Charge-Off?

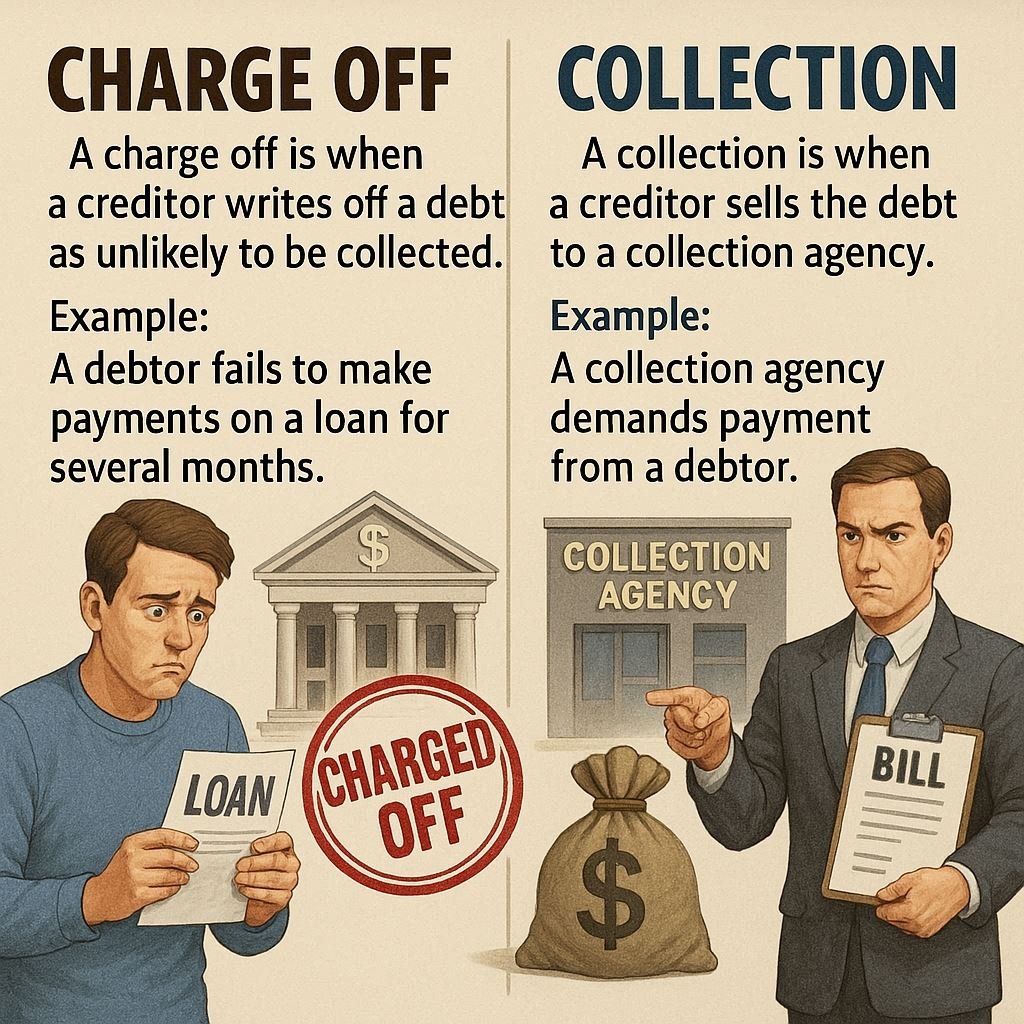

A charge-off happens when a creditor (like a credit card company or lender) decides your debt is unlikely to be collected. Typically, this happens after you’ve missed payments for 180 days or more. The creditor will “write off” the debt for accounting purposes, but that doesn’t mean you no longer owe it. The debt can still be collected, either by the original creditor or by a third-party collection agency.

Key things to know about charge-offs:

- It usually occurs after 6 months of nonpayment.

- It remains on your credit report for up to 7 years from the date of first delinquency.

- You still legally owe the debt.

- It can be sold or transferred to a collection agency.

What Is a Collection?

A collection is when your unpaid debt is turned over to a collection agency. This can happen either after a charge-off or in some cases before the creditor officially charges off the debt. The collection agency’s job is to recover the money you owe, and they can contact you directly through calls, letters, or even emails.

Key things to know about collections:

- It can happen before or after a charge-off.

- Collection accounts also remain on your credit report for up to 7 years.

- Paying the collection won’t instantly remove it unless you negotiate a “pay-for-delete” agreement.

- Multiple collection agencies can end up owning the same debt at different times.

Learn how to handle debt collectors and how to get debt collectors to stop calling.

Side-by-Side Comparison

| Charge-Off | Collection |

|---|---|

| Creditor writes off the debt for accounting purposes | Debt is sent to a third-party agency for collection |

| Happens after about 180 days of missed payments | Can happen before or after a charge-off |

| Reported by original creditor | Reported by the collection agency |

| Debt still owed | Debt still owed |

| Can be sold or transferred to collections | Collection attempts can include calls, letters, and legal action |

How These Affect Your Credit Score

Both charge-offs and collections can severely impact your credit score, especially if your score was in good standing before. A single negative mark can drop your score by dozens (or even hundreds) of points. While time and positive payment history can reduce their impact, they will still appear on your report for years unless removed.

What to Do If You Have a Charge-Off or Collection

- Verify the debt: Make sure the account information is accurate and belongs to you.

- Negotiate: In some cases, you can work out a payment plan or a lump-sum settlement.

- Ask for pay-for-delete: Some collectors will remove the account from your report in exchange for payment (get it in writing first).

- Dispute errors: If the information is wrong, file a dispute with the credit bureaus.

- Read this post on removing collections from your credit report.

Final Thoughts

While a charge-off and a collection are different, they both signal serious delinquency and can have a long-lasting effect on your credit. The sooner you take action — whether that’s negotiating, paying, or disputing — the better your chances of minimizing the damage.

For more details on how credit reports work and how to improve your score, visit the Federal Trade Commission’s guide on credit repair.